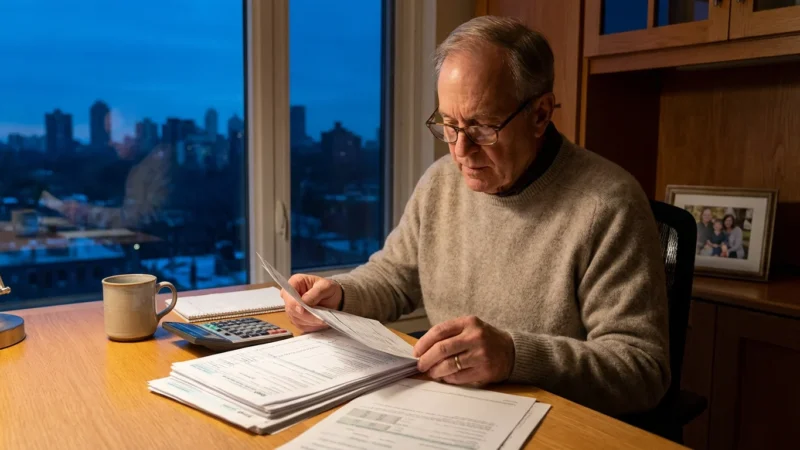

Social Security forms a foundational pillar of many Americans’ retirement income. Understanding how these benefits work, when to claim them, and how they fit into your broader financial picture is crucial for a secure future. Your Social Security income is not a standalone element, but a vital component that interacts with your savings, investments, and other income sources. Thoughtful retirement planning integrates Social Security benefits to optimize your financial stability.

Understanding Your Social Security Benefits

Social Security benefits derive from your lifetime earnings. The Social Security Administration (SSA) calculates your Primary Insurance Amount (PIA) using your highest 35 years of indexed earnings. This PIA represents the amount you receive if you claim benefits at your Full Retirement Age (FRA). Your FRA depends on your birth year. For example, if you were born in 1960 or later, your FRA is 67.

You can start claiming benefits as early as age 62, but doing so reduces your monthly payment permanently. Waiting past your FRA, up to age 70, increases your monthly benefit. These delayed retirement credits can significantly boost your income, accumulating at 8% per year for each year you delay past FRA.

Knowing your benefit statement is the first step toward effective retirement planning. You can access your personalized statement online through your my Social Security account. This statement provides estimated benefits at various claiming ages, helping you visualize your potential income streams.

The best time to plant a tree was 20 years ago. The second best time is now.

When to Claim: Impact on Your Financial Plan

Deciding when to start your Social Security benefits is one of the most critical decisions you make for your retirement. This choice directly impacts your monthly income for the rest of your life. Claiming early, at age 62, might seem appealing for immediate cash flow, but it reduces your monthly payment by up to 30% compared to claiming at your FRA. For instance, if your FRA benefit is $2,000, claiming at 62 might reduce it to $1,400.

Before finalizing your strategy, it is wise to review common Social Security myths that might affect your decision-making process.

Conversely, delaying benefits past your FRA increases your monthly payment. For someone with an FRA of 67, delaying until age 70 can result in a monthly payment 32% higher than their FRA amount. Using the previous example, a $2,000 FRA benefit could become $2,640 per month at age 70. This increase provides a powerful hedge against inflation and longevity risk.

Your claiming strategy should align with your personal financial situation, health, and life expectancy. Consider your need for income, your other retirement savings, and your family’s financial needs. There is no one-size-fits-all answer, so evaluate your options carefully.

Factors influencing your claiming decision include:

- Current income needs: Do you need the money now to cover essential living expenses?

- Other retirement savings: Can your 401(k)s, IRAs, or pensions support you until a later claiming age?

- Health and life expectancy: If you expect a shorter lifespan, claiming earlier might provide more total benefits. If you anticipate a long life, delaying generally yields more overall.

- Spousal benefits: Your claiming decision affects your spouse’s potential survivor benefits.

- Desire to work: If you plan to continue working, claiming early might lead to a reduction in benefits due to earnings limits.

Estimating Your Future Benefits

Accurate benefit projections are essential for robust retirement planning. The Social Security Administration provides several tools to help you estimate your future benefits. These tools give you a clear picture of what you can expect at different claiming ages.

The most important tool is your personalized Social Security Statement. You can access this statement by creating a my Social Security account online. Your statement provides a detailed earnings history and estimates your future benefits at age 62, your Full Retirement Age, and age 70. Review your earnings record regularly to ensure accuracy, as errors can impact your future benefits.

Another valuable resource is the SSA’s online Retirement Estimator. This tool allows you to plug in different retirement dates and earnings scenarios. You can see how various factors, such as working longer or earning more, affect your monthly payment. This interactive approach helps you explore different financial plan scenarios.

Steps to estimate your benefits:

- Create a my Social Security account: Visit the official SSA website to set up your secure online account.

- Review your earnings record: Check for any inaccuracies in your reported earnings. Report any missing or incorrect information immediately.

- Use the Retirement Estimator: Experiment with different claiming ages to see the impact on your monthly benefit.

- Consider your spouse’s benefits: If married, understand how your claiming decision might affect your spouse’s spousal or survivor benefits.

- Update projections periodically: Revisit your estimates every few years as your earnings and circumstances change.

Coordinating Social Security with Other Retirement Income

Your financial plan thrives when all its components work together. Social Security should integrate seamlessly with your other retirement income sources. This holistic approach ensures you maximize your financial security and meet your retirement goals.

Don’t forget to account for healthcare; understanding the connection between Social Security and Medicare is vital for accurate long-term budgeting.

Many retirees rely on a combination of income streams. These commonly include personal savings, such as 401(k)s and IRAs, pensions, and Social Security benefits. How you time your Social Security claims can impact how quickly you draw down your other assets. For example, delaying Social Security until age 70 might require you to rely more heavily on your savings in your early retirement years. However, the larger monthly Social Security payment later can make your savings last longer overall.

Consider the role of Social Security as a fixed, inflation-adjusted income stream. Unlike market-dependent investments, Social Security provides a predictable benefit that typically includes annual cost-of-living adjustments (COLAs). This predictability makes it an excellent foundation for covering essential expenses, reducing the need to draw heavily from volatile investment accounts during market downturns. According to the Social Security Administration, COLAs help maintain the purchasing power of benefits over time.

When coordinating income, think about:

- Your spending plan: Identify your essential and discretionary expenses. Use Social Security to cover a significant portion of your essential needs.

- Investment withdrawal strategy: Determine how Social Security impacts your safe withdrawal rate from your investment portfolio. A higher Social Security benefit might allow for a lower withdrawal rate from your savings, helping your principal last longer.

- Pension integration: If you have a pension, understand how it combines with Social Security to meet your overall income needs. Some pensions may be subject to offsets if you also receive Social Security.

- Part-time work: If you plan to work part-time in retirement, understand how your earnings might affect your Social Security benefits if you claim before your Full Retirement Age.

Strategies for Maximizing Your Social Security

Maximizing your Social Security benefits involves more than just picking a claiming age. It requires strategic thinking about your earnings history, marital status, and other financial resources. These strategies aim to secure the highest possible lifetime benefits for you and your family.

One key strategy involves working for at least 35 years. The SSA uses your 35 highest-earning years to calculate your benefit. If you have fewer than 35 years of work, those non-working years count as zero, lowering your overall average. Extending your career, even part-time, can replace low-earning years with higher ones, boosting your average.

Another powerful strategy is delaying your claim. Each year you delay claiming Social Security past your Full Retirement Age, up to age 70, you earn delayed retirement credits. These credits increase your monthly benefit by 8% per year. For example, if your FRA is 67 and you delay until 70, your monthly benefit will be 24% higher than at FRA. This often provides the most significant increase in individual benefits.

For married couples, coordinated claiming strategies are especially beneficial. One common approach involves the higher earner delaying their benefits until age 70, maximizing their individual benefit. The lower-earning spouse might claim spousal benefits or their own benefit earlier, providing some income while the higher earner’s benefit grows. This strategy can also increase the survivor benefit for the remaining spouse.

Key strategies to consider:

- Work at least 35 years: Ensure you replace any low-earning years with higher ones.

- Maximize your earnings during peak years: Higher earnings translate to higher benefits.

- Delay claiming benefits until age 70: If health and financial circumstances allow, this provides the largest monthly payment.

- Coordinate with your spouse: Explore spousal and survivor benefit options to maximize household income.

- Monitor your earnings record: Regularly check your my Social Security account for accuracy.

Integrating Social Security into Your Overall Financial Plan

Social Security is not a standalone income stream, but a crucial component of your comprehensive retirement strategy. Effective integration means viewing your Social Security benefits as part of a larger financial ecosystem, including your savings, investments, and expenses. This integrated perspective helps you build a resilient and sustainable retirement plan.

You should also account for how your benefits are taxed at both federal and state levels to determine your true net income.

A comprehensive approach involves managing your budget effectively to ensure these benefits cover your primary lifestyle needs.

Start by projecting your estimated Social Security income at different claiming ages. Then, subtract this income from your total anticipated retirement expenses. The remaining gap represents the amount you need to cover from your other savings and investments. This exercise clarifies how much you rely on your personal savings and helps you determine a sustainable withdrawal rate from your portfolio.

Consider Social Security as your “floor” income, covering your basic living expenses. This approach allows your more volatile investment accounts to grow for longer or to be used for discretionary spending. By minimizing early withdrawals from investments, you give them more time to compound, enhancing your long-term financial security. Your financial plan benefits from this stable base.

Integrating Social Security involves:

- Creating a detailed budget: Understand your fixed and variable expenses in retirement.

- Calculating your income gap: Determine how much Social Security covers and how much more you need from other sources.

- Developing a withdrawal strategy: Plan how and when you will draw from your 401(k)s, IRAs, and other savings, factoring in your Social Security income.

- Considering inflation: While Social Security provides COLAs, factor general inflation into your long-term expense projections.

- Seeking professional advice: A qualified financial advisor can help you create a personalized integration strategy.

Considering Taxation of Social Security Benefits

Many retirees are surprised to learn that a portion of their Social Security benefits can be subject to federal income tax. The amount of your benefits that is taxable depends on your “provisional income.” Understanding this can significantly impact your retirement budget and overall financial plan.

Depending on your combined income, it is essential to understand the taxation of your benefits to properly forecast your net retirement income.

Provisional income includes your adjusted gross income, any tax-exempt interest, such as from municipal bonds, and one-half of your Social Security benefits. If your provisional income exceeds certain thresholds, a percentage of your benefits becomes taxable. For single filers, if your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it is over $34,000, up to 85% may be taxable. For married couples filing jointly, these thresholds are $32,000 and $44,000.

Some states also tax Social Security benefits. Currently, a minority of states do. Check your state’s tax laws to understand the full tax implications for your benefits. This information is vital for accurate budgeting and tax planning in retirement. You can find detailed guidance on taxation from the IRS.

To manage potential taxation:

- Estimate your provisional income: Calculate this annually to anticipate your tax liability.

- Consider tax-efficient withdrawals: Strategize withdrawals from different account types, taxable, tax-deferred, tax-free, to manage provisional income.

- Consult a tax professional: A tax advisor can help you understand specific implications and plan accordingly.

- Withhold taxes: You can choose to have federal income tax withheld from your Social Security benefits, or pay estimated taxes.

Protecting Your Social Security Benefits from Scams

Unfortunately, scammers often target older adults, attempting to steal their Social Security benefits or personal information. Staying vigilant and informed is your best defense against these fraudulent schemes. Protecting your identity and finances ensures your Social Security income remains secure.

Always remember that the SSA will never call to threaten you, so learning how to prevent common scams is the best way to safeguard your future.

One common scam involves callers or emails impersonating Social Security Administration employees. They might claim your benefits are suspended, your account has been compromised, or that you owe money. Often, they demand personal information, gift cards, or wire transfers. The SSA will never call you and demand immediate payment, threaten arrest, or ask for gift cards or wire transfers.

You should also be wary of phishing attempts. These are emails or texts that look official but try to trick you into clicking malicious links or revealing sensitive data. Always verify the sender and never click on suspicious links. If you suspect a scam, contact the SSA directly using their official contact information found on ssa.gov, not a number provided by the suspicious caller or email.

Tips for protecting your benefits:

- Be skeptical of unsolicited calls and emails: The SSA typically communicates via mail for official business.

- Never share personal information: Do not give out your Social Security number, bank account details, or other sensitive information over the phone or email unless you initiated the contact and verified the recipient.

- Hang up on threatening calls: Scammers often use intimidation tactics.

- Report suspicious activity: If you receive a scam call or email, report it to the SSA Office of the Inspector General.

- Create a strong my Social Security account: Secure your online account with a strong password and multi-factor authentication.

Frequently Asked Questions

Can I work and still receive Social Security benefits?

Yes, you can work and receive Social Security benefits. However, if you are under your Full Retirement Age, the SSA has earnings limits. If your earnings exceed these limits, they will temporarily withhold a portion of your benefits. Once you reach your Full Retirement Age, these earnings limits no longer apply, and you can earn any amount without your benefits being reduced.

How does divorce affect Social Security benefits?

If you were married for at least 10 years, are currently unmarried, and are age 62 or older, you may be able to claim benefits on your ex-spouse’s record. This applies if your ex-spouse is entitled to Social Security retirement or disability benefits. Your benefits as a divorced spouse do not affect the benefits your ex-spouse or their current spouse receives.

What happens to my Social Security benefits if I become disabled?

Social Security provides disability benefits for those who cannot work due to a severe medical condition expected to last at least one year or result in death. If you qualify for Social Security Disability Insurance (SSDI), your retirement benefits would typically convert to disability benefits. The eligibility criteria and application process differ from retirement benefits, but they draw from the same earnings record.

Do Social Security benefits receive Cost-of-Living Adjustments (COLAs)?

Yes, Social Security benefits typically receive annual Cost-of-Living Adjustments (COLAs). Congress bases these adjustments on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). COLAs aim to ensure that the purchasing power of your benefits keeps pace with inflation, helping to maintain your standard of living in retirement.

Can I change my mind after I start receiving Social Security benefits?

Yes, in certain circumstances, you can withdraw your application for Social Security benefits. You have up to 12 months after starting benefits to withdraw your application. You must repay all benefits you received, including any benefits paid to your family based on your record. You can then reapply for benefits at a later date, potentially at a higher amount due to delayed retirement credits.

Disclaimer: This article is for informational purposes only. Benefits, programs, and regulations can change. We encourage readers to verify current information with official government sources and consult with qualified professionals for personalized advice.

Leave a Reply